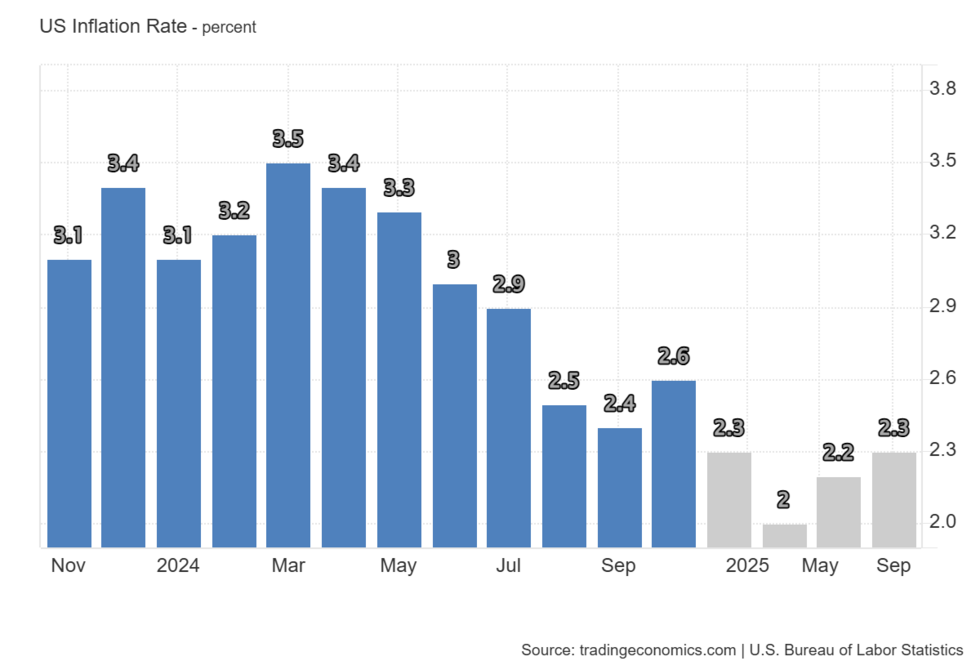

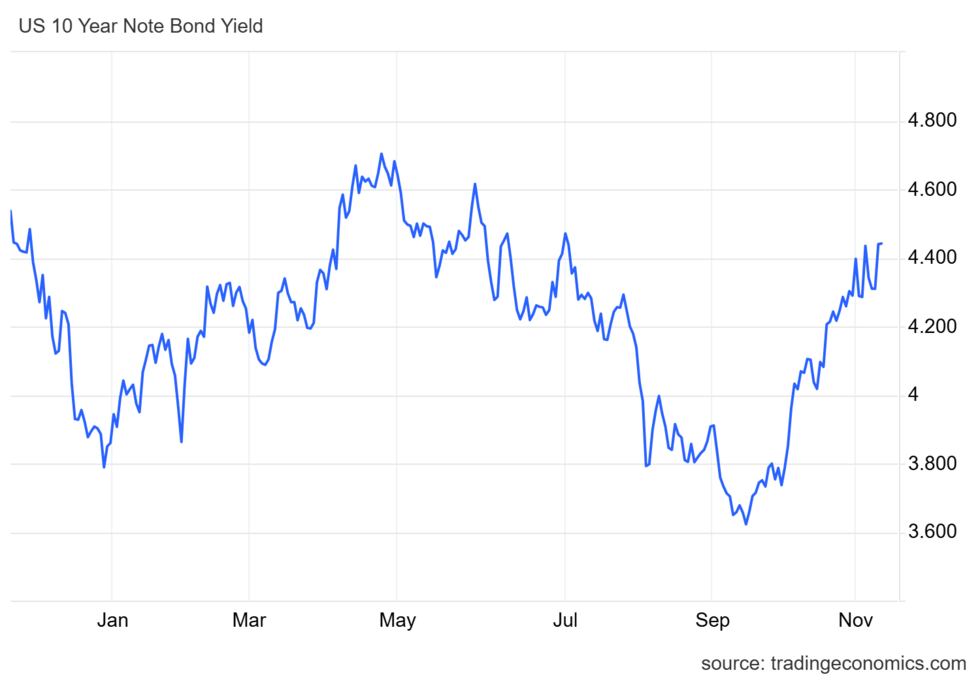

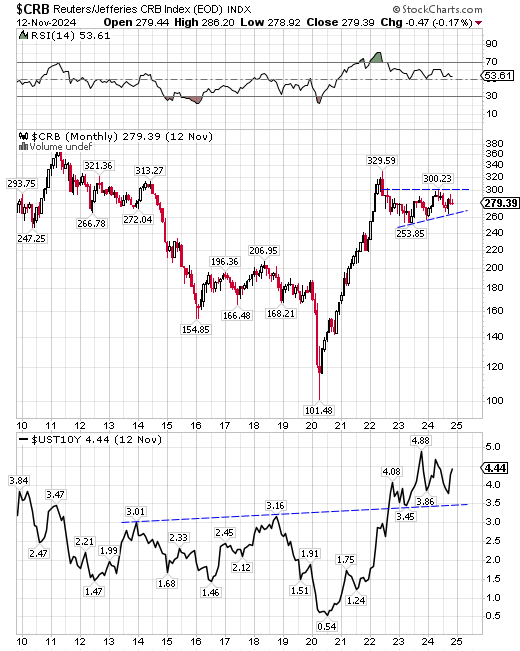

November 13, 2024: Inflation persistsThe annual inflation rate in the U.S. accelerated in October to 2.60%, the first uptick in seven months. Traders are reviewing the latest data, which suggests this bump-up is not the start of a new upward trend but rather an indication of just how persistent inflationary pressure is (Chart 1). The core consumer inflation rate is also showing a rise after 15 months of steady declines. Advancing slightly faster than expected in September and October, reflecting the increase in shelter and transportation costs. Inflationary pressure is driving other asset groups higher. The U.S. 10-year T-bond yields (Chart 2) have moved to a four month high of 4.44% limiting the Fed's rate cutting cycle in December. Treasuries remain under pressure as the expected impact of Trump's economic policies risk a continued hawkish response from the central bank. The outlook on bond yields also influences the commodity market. The CRB continues to move in lock-step with the US 10-year yields (Chart 3). Inflation expectation plays a big role in trader's decisions. At present both the CRB and bond yields are stalling after advances in 2023 and 2024. Bottom line: US inflationary pressure is more challenging to remove than most economists and analysts predicted. The expected agenda from the in-coming president is only adding to trader's already hawkish outlooks. Our models suggest the US inflation rate should remain between 2.20% and 2.30% into early 2025. 10 year T-bond yields are anticipated to hold around 4.40% and the CRB remaining well supported and retest the 300 level. |    |

|

|

|

|

D.W. Dony and Associates

4973 Old West Saanich Rd.

Victoria, BC

V9E 2B2

|